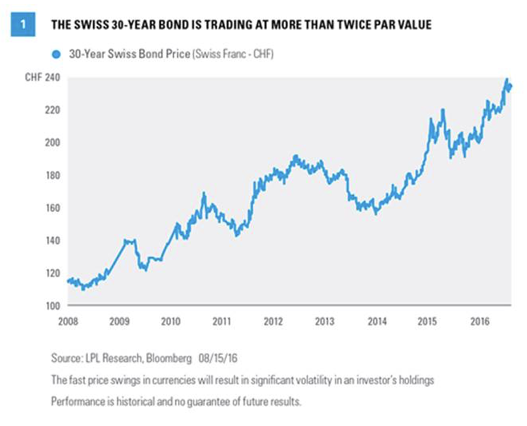

Slow global growth and low or negative interest rate policies from major central banks make for a difficult environment for income investors. U.S. yields are low relative to history, but overseas investors have it even worse, with central banks in many developed nations pursing negative interest rate policies that have pushed government bond prices to all-time highs. Figure 1 shows the price of one such bond, the 30-year Swiss government bond, which is currently trading at a price of 235 Swiss francs, more than double the typical “par” price of 100 that results in an investor receiving the stated coupon on a bond.

U.S. Treasuries and other government bonds may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit and market risk. U.S. Treasuries are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

SAFETY ISN’T CHEAP

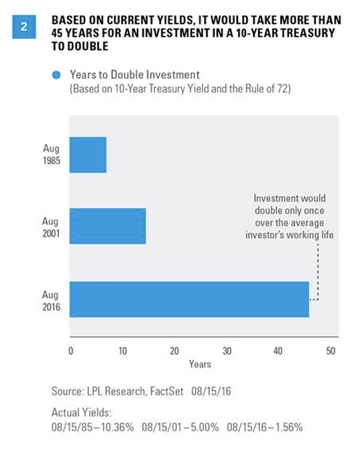

U.S. Treasury yields are higher than their foreign counterparts, but yields have been on a downward trajectory for more than 30 years. The rule of 72 is a common shortcut in which 72 is divided by an investment’s annual return to determine the number of years it will take for an investor’s money to double. Thirty-one years ago, in August 1985, investors were able to receive a yield of more than 10% on a 10-year Treasury, allowing their money to double in approximately 7 years with very little risk of default. Moving forward to 2001, the 10-year Treasury yielded closer to 5%, meaning it would take 14 years for an investor’s money to double. Fast-forward to 2016, and it would now take more than 45 years to double an investment in a 10-year Treasury [Figure 2], or put another way—the investment would double only once during the average investor’s working life.

The rule of 72 is a mathematical concept and does not guarantee investment results nor functions as a predictor of how an investment will perform. It is an approximation of the impact of a targeted rate of return. Investments are subject to fluctuating returns and there is no assurance that any investment will double in value.

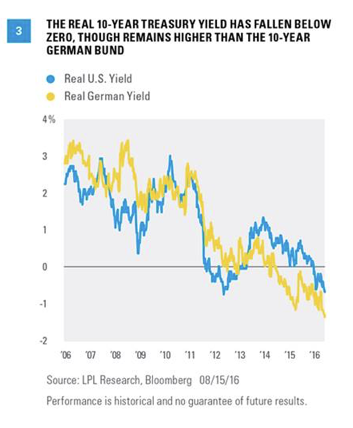

Though nominal yields remain well above zero in the U.S., real yields (yields adjusted for the impact of inflation) have fallen into negative territory, though not as far as other developed nations, such as Germany [Figure 3].

The grab for yield has led to above-average valuations not only in the bond market, but also in some areas of the equity market. Sectors such as utilities, consumer staples, and real estate investment trusts (REIT) have seen strong year-to-date gains (19.7%, 10.4%, and 15.5%, respectively[1]), and price-to-earnings ratios (PE) for the former two sectors are near post-crisis highs [Figure 4]. The PE ratio of the S&P 500 utilities sector, at 18.7, is well above its post-1990 average of 14.8, and the consumer staples sector is at an even higher multiple of 23, versus a post-1990 average of 19.8. Forward valuations, measured by price to funds from operations (PFFO), for the REIT sub-sector of the S&P 500 (which will soon become a sector of its own), are also toward the top of their post-crisis range. All three sectors continue to offer a higher level of income than the overall S&P 500, and distribution levels for the REIT sub-sector have actually increased slightly year to date; although utilities and consumer staples have seen yields fall more quickly than those of the overall S&P 500 year to date, as valuations have increased.