How can that happen? If I buy producing wells out of bankruptcy at $.10 on the dollar, then my cost of production just dropped by 90%. I know, I know, it can’t happen, right? Think Global Crossing. They laid thousands of miles of fiber optic under the oceans at immense cost, which auctioned off for pennies on the dollar. We should all be grateful to those unlucky investors, because they are why you and I can now enjoy cheap Internet and telecommunication prices. Why should oil be any different?

I’ve said for a long time that the entire “Peak Oil” thesis was wrong. I believe that more now than ever. Far from running out of oil, the world has way too much of it. We will be dealing with the consequences for years to come.

This story literally just came across on Bloomberg:

Markets are currently in a well-oiled “death spiral,” according to Citigroup Inc. analysts led by Jonathan Stubbs.

“It appears that four inter-linked phenomena are driving a negative feedback loop in the global economy and across financial markets,” the analysts write, citing the resilient US dollar, lower commodities prices, weaker trade and capital flows, and declining emerging market growth.

“It seems reasonable to assume that another year of extreme moves in US dollar (higher) and oil/commodity prices (lower) would likely continue to drive this negative feedback loop and make it very difficult for policy makers in emerging markets and developing markets to fight disinflationary forces and intercept downside risks,” the analysts add. “Corporate profits and equity markets would also likely suffer further downside risk in this scenario of Oilmageddon.”

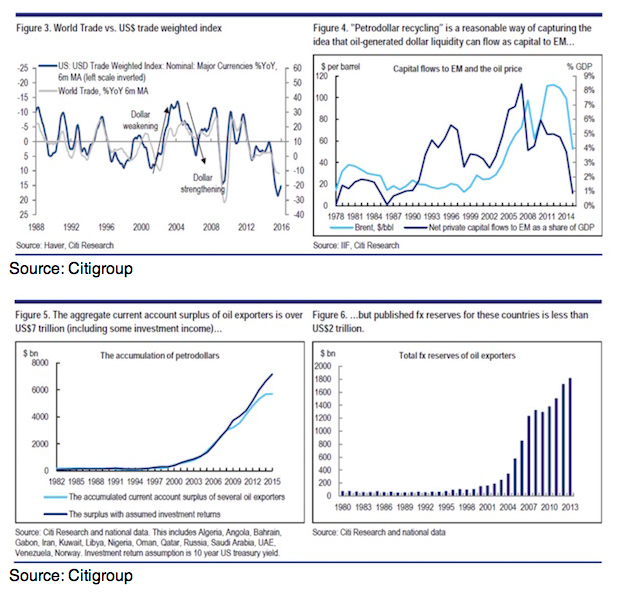

Their case is bolstered by a collection of charts showing the linkages between the four factors cited above, including the importance of lofty oil prices to the ready supply of petrodollars circulating in the world economy and flowing to financial assets. Oil exporters have enjoyed more than $6 trillion flowing into their current accounts, according to Citi’s estimates, implying some $4 trillion of capital in sovereign wealth funds (SWFs).

“But, the collapse in oil/commodity prices and sharp fall in the pace of world trade means that these same economies will likely experience an aggregate current account deficit for the first time since 1998,” says Citi. “In turn, this is likely to put pressure on SWF and broader emerging market liquidity as governments and emerging market economies would need to ‘lean’ on reserves in order to maintain economic, political and social stability. This has clear feedback loops across emerging markets.”

Accordingly, the impact of the feedback loop is being felt far and wide in financial markets, extending even to US inflation expectations. Where once 10-year inflation breakevens had little relationship with the price of oil, they have for the past two years moved in tandem.