There is a broad consensus that equities are in a “low return environment”. Although such fears might have been expected following 2008’s bear market, it is surprising that the low-return rhetoric continues despite that the bull market is now more than 7 years old.

Richard Bernstein is chief executive and chief investment officer at Richard Bernstein Advisors.

Fears that returns would be lower than normal have fostered grave misperceptions that have hurt overall portfolios’ performance. Despite investors’ fears, this cycle’s returns have actually been quite normal over various time horizons.

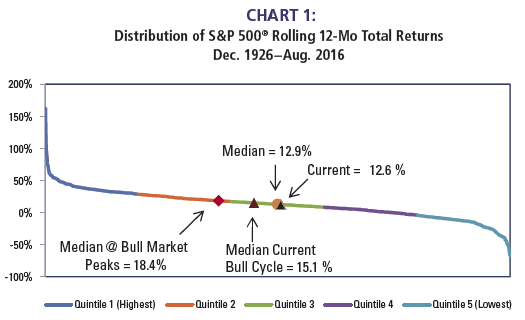

Chart 1 shows the distribution of all rolling 12-month total returns from December 1926 onward delineated by quintile. The most recent 12-month return of 12.6% looks normal, sitting just slightly below the median of 12.9%.

Source: Richard Bernstein Advisors LLC, Standard & Poor’s, Morningstar For Index descriptors, see "Index Descriptions" at end of document. Past performance is no guarantee of future results.

This cycle’s median 12-month return does not appear extreme or over-heating of the bull market. Although easily above the long-term median, the current bull market’s median 12-month return of 15.1% remains in the middle quintile historically, whereas the typical median total return at stock market peaks was 18.4%.

Longer-term performance appears quite normal – Neither too hot nor too cold

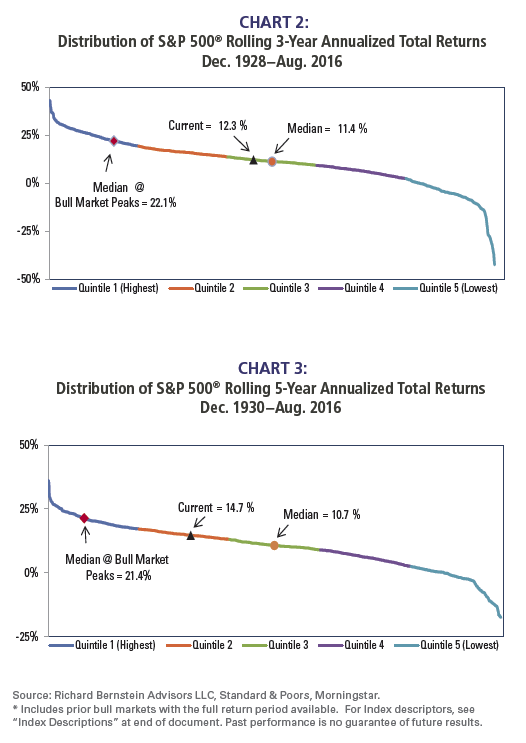

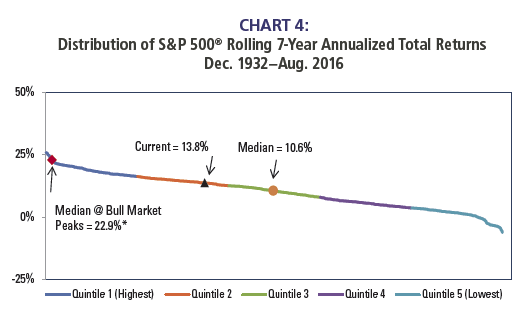

Over either a 3-year, a 5-year or a 7-year annualized horizon, the returns distribution charts below also highlight that current returns look normal. Each period’s returns are above their long-term median. However these returns certainly do not suggest the euphoric excess that has typically accompanied prior bull market peaks.

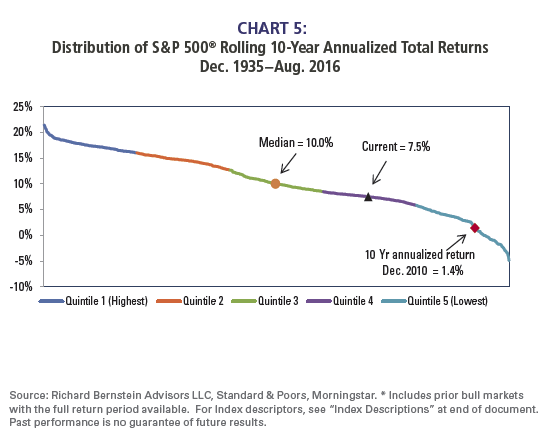

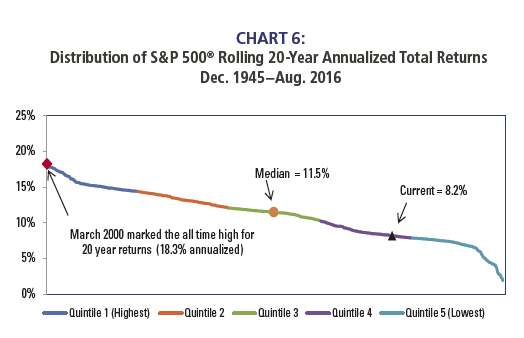

When examining a 10- or 20-year time horizon, one can see the impact of the “lost decade” (i.e . the low return environment of the 2000’s). Annualized returns drop well below the median for these time horizons.

Source: Richard Bernstein Advisors LLC, Standard & Poors, Morningstar. For Index descriptors, see "Index Descriptions" at end of document. Past performance is no guarantee of future results.

A low return environment or simply poor asset allocation choices?

Although it is widely accepted that equities are mired in a period of low returns, the data suggest the rhetoric appears to be a significant misperception. Actual returns appear to be quite normal (i.e., neither too hot nor too cold) for the ongoing bull market, regardless of the time horizon reviewed.

While it is true that historical returns that incorporate 10 and 20 years appear well below normal, those inferior returns appear to be attributable to the “lost decade” of the 2000s and not to the current cycle’s returns. In other words, the so-called low return environment already occurred and equity returns are returning to normal.

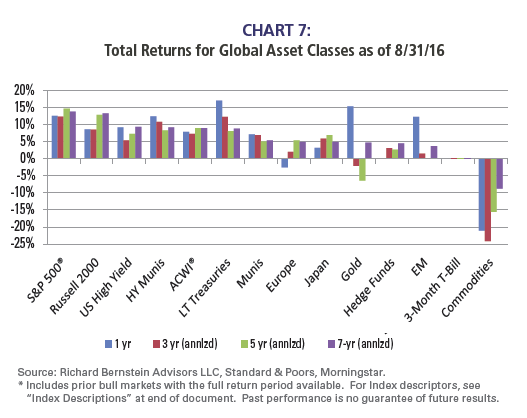

Chart 7 on the next page shows major asset class performance over the past 1,3,5 and 7-year time horizons. Clearly US equities have had strong absolute as well as strong relative performance over each of these periods. However a number of asset classes have not fared well at all. It appears the misperception that low returns are the ongoing norm may merely be the result of investors’ poor asset allocation decisions over the past several years.

The opportunity cost of misperception and poor asset allocation has been very high. Both institutional and individual investors have largely missed out on an annualized return of roughly 14% in the past seven years in the US equity market, and recent surveys and flow of funds suggest investors generally remain wallflowers.

It appears as though there is nothing “new” about the “new normal”. It’s simply “normal”.

'New Normal': Not New. Just Normal.

September 14, 2016

« Previous Article

| Next Article »

Login in order to post a comment