Is global aging about to end the savings glut? Some observers think so. More and more baby boomers are reaching retirement age, and they will soon not only save less but also start to dump their accumulated assets to fund retirement … or so the story goes. If this were true, the consequences for interest rates would be profound. The real long-term equilibrium interest rate, which has been on a secular downtrend for decades partly due to strong working-age cohorts saving hard for retirement, would start to rise – and what we here at PIMCO call The New Neutral might soon be history.

We strongly disagree with that thesis of an imminent demographics-induced savings drought. Rather, we have argued in recent work that the global excess supply of saving over investment, which has been largely responsible for the secular decline in equilibrium interest rates, is not only here to stay but likely to increase further in the coming years for a host of reasons including demographics (see PIMCO Macro Perspectives, “No End to the Savings Glut,” September 2015). As a consequence, we continue to expect the fundamental forces of elevated desired saving to keep the equilibrium real rate depressed and to limit the extent to which other (cyclical) factors can drive up market interest rates.

However, given the popularity of the thesis that demographics will soon end the savings glut, we undertook a deep dive into the data to investigate the link among demographics, saving behavior and the demand for fixed income assets – with some surprising results. Here’s what we found.

A ‘demographic reversal?’ Not so fast!

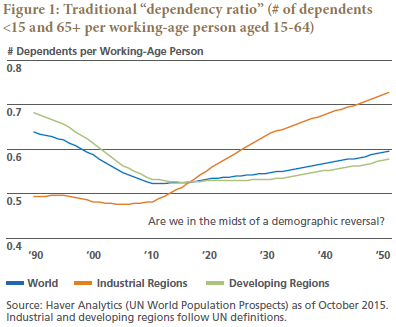

People of the world, we’re getting old. It’s a well-known fact that, after decades of decline, the global dependency ratio – traditionally defined as the ratio of individuals younger than 15 and older than 64 to the working-age population aged 15-64 – is now rising (see Figure 1).

Some financial market observers argue that this demographic trend reversal will begin to drive interest rates higher, and soon. Why? First, a declining share of high-saving workers and a rising share of dissaving elderly will (the argument goes) erode the demand for saving – and drive interest rates higher via the savings-investment equilibrium. Second, these observers argue, a rapidly growing share of retirees will have to consume (i.e., sell down) their financial asset holdings to fund spending in retirement, and these drawdowns will create selling pressure in financial markets that pushes asset prices down and interest rates up.

Our core thesis in a nutshell: Yes, global aging may someday drive U.S. interest rates structurally higher. But “someday” remains at least a decade away – for two reasons. First, we proffer that global saving will remain stronger than many expect, supporting a low global neutral interest rate. (As investors, we care about the neutral rate because it anchors fixed income yields in the market.) Second, U.S. demographic demand for fixed income assets should remain robust until at least 2025 – and in the meantime should continue to put downward pressure on market yields, all else equal. Combine a low global “anchor” and strong domestic fixed income demand, and what do you get? Lower rates for longer in the U.S.

Continuing robust demographic demand for saving

Remember the link between saving and interest rates: In the savings-investment equilibrium, rising demand for saving pushes down the equilibrium (or neutral, or natural) rate of interest, all else equal, and vice-versa. Our task, then, is to assess how demographic changes affect aggregate saving. We find that the traditional “dependency ratio,” used in many other studies on this topic, is flawed. We suggest two modifications to address those flaws. First, the young, considered “dependents,” contribute very little to global saving and dissaving in dollar terms (they’re “non-savers”). We therefore prefer to focus on the ratio of “Peak Savers” (mature adult workers who earn and save a lot) to “Elderly” (who save less as they age and ultimately consume their savings in retirement). Let’s preliminarily define “Peak Savers” as individuals aged 35 to 64, for two reasons:

• People 35–64 have generally exhibited much higher savings rates than people in younger and older age groups;

• People 35–64 earn considerably more income than people younger and older – so for any given savings rate, this age group’s saving behavior will have an outsized effect on saving and investment flows in dollar terms.

Let’s preliminarily define “Elderly” as everyone 65 and older (the traditional definition). Thus, the global Peak Savers versus Elderly ratio in Figure 2 reflects a static 35–64 Peak Saver cohort – and reveals what appears to be a demographic cliff in about year 2010. Those who argue that demographic support for saving will fall sharply in the coming years typically will try to prove their point using a ratio like this one.