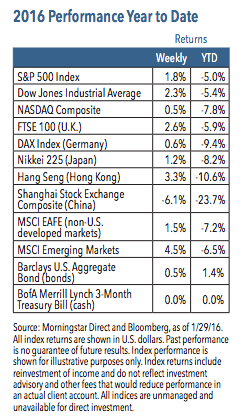

Volatility remained high last week as U.S. equities regained some ground, with the S&P 500 Index rising 1.8%. Stocks soared on Friday in response to the Bank of Japan’s decision to adopt a negative interest rate stance. Oil prices also rose over speculation that global production might fall. Corporate earnings were mixed, as results continued to be held back by the long-term decline in lower oil prices, a soft economic backdrop and the strong dollar.

Weekly Top Themes

1. Fourth quarter gross domestic product growth was soft. The economy grew an anemic 0.7% last quarter, with growth held back by slowing consumer spending and the first decline in business investment since 2012. A slowdown in inventory investment also detracted from results. For the year as a whole, 2015 growth increased a respectable 2.4%, matching the pace seen in 2014.2

2. Last week’s Fed meeting came with no real surprises as the central bank adopted a slightly more dovish tone. The Fed noted somewhat weaker economic growth, but also sounded upbeat about demand and employment indicators. Policymakers also indicated that inflation remains low and stated they were “closely monitoring global economic and financial developments.”

Absent a quick and dramatic economic improvement, we do not expect another interest rate increase before June.

3. The energy sector continues to weigh on corporate earnings. With over half of companies reporting fourth quarter results, earnings are beating expectations by 4.9% and revenues are missing by 0.3%. Earnings-per-share are on track to

be flat for the quarter, and up about 6% excluding energy.

4. Consumer confidence may be slowly improving. The Conference Board’s Consumer Confidence Index increased 1.8 points in January, beating expectations. Consumers may be looking past equity market weakness and focusing on the positives.

5. The anticipated “oil dividend” has yet to appear. Since oil prices started falling in 2014, many observers (us included) expected to see an increase in consumer and business spending. It doesn’t appear that this has yet occurred, and it looks to us as if most individuals are saving their extra disposable income rather than spending it. We expect consumer spending to rise, but acknowledge that lower oil prices have so far caused more pain than benefits.

A Pro-Growth Stance Makes Sense, but Requires Patience Investors have grown more risk-averse in recent weeks with slowing growth in China, oil price volatility, weakness in manufacturing and Fed policy topping the list of concerns. Economic data has generally been stronger than reflected by financial market movements, and investors seem to be ignoring positive economic news and overly focusing on the negatives.

At this juncture, we think investors have three options: (1) retreat and unload risk assets in anticipation of a recession, (2) pause, become slightly more conservative and await more clarity, or (3) maintain a pro-growth stance and accept that more

near-term turbulence may occur before risk assets experience a sustained upturn.

We think the first strategy is overly pessimistic and believe economic fundamentals are better than what is priced into the market. The second option may be reasonable for investors who are having difficulty weathering the current volatility. But for investors with long-term time horizons, we think option three is most prudent.

It may take some time, but we expect that oil prices should stabilize and cease being the main determinant of global financial market prices. The long-term drop in oil should produce some economic stimulus and become more of a positive. Additionally, global monetary policy remains a tailwind for risk assets. The Fed is likely to raise rates, but any increase should be measured and slow. And last week’s news from Japan reiterates that policy around the world remains in easing mode. Investors are also awaiting signs of a global manufacturing recovery, which would promote greater confidence in the strength of the world economy. Our view is that financial markets have overreacted to the negatives. Turbulence is likely to continue, but we expect both equity prices and bond yields to rise over the

course of 2016.