As U.S. corporations begin to report their results for the recently completed first quarter of 2016, global growth will likely take center stage among investors. While comments from corporate managements on business conditions in Europe, Japan, China, and other emerging markets will be closely watched, those comments may be overshadowed. This week, the International Monetary Fund (IMF) will publish the spring edition of its World Economic Outlook publication. In addition, Christine Lagarde, the managing director of the IMF, will garner plenty of attention in the financial media, as she briefs investors on the publication and prepares for the IMF-World Bank spring meetings in Washington, DC. Although we don’t know what the IMF will forecast for global growth, if history is any guide, the global gross domestic product (GDP) forecasts for 2016 and 2017 should be lower than the forecasts made by the IMF last fall. Lagarde is also likely to remind policymakers (and investors) that central banks (via monetary policy) cannot boost global growth alone, and that fiscal policy is also required. Aside from a few countries, our view is that the call for more fiscal policy will go unheeded.

WHY GLOBAL GDP GROWTH MATTERS

The outlook for global growth matters to investors because it defines the ultimate pace of activity that creates value for countries, companies, and consumers.

As investors begin to digest the S&P 500 earnings reports for the first quarter of 2016 (15 S&P 500 companies will report first quarter results this week, with another 300 set to report in the final two weeks of April 2016), we provide an update on how consensus estimates for economic growth for 2016 and 2017 — in the United States and worldwide — have evolved over the past few years.

In recent years, markets have focused more on global GDP growth, whereas in the past, prospects for U.S. economic growth garnered the most attention from market participants. Why does global GDP growth matter? As we have noted in prior Weekly Economic Commentaries, financial markets — especially equity markets — focus intently on earnings. Broadly speaking, earnings growth is driven by “top-line” growth, or revenue growth, less the costs incurred earning that revenue, with labor accounting for more than two-thirds of total costs.

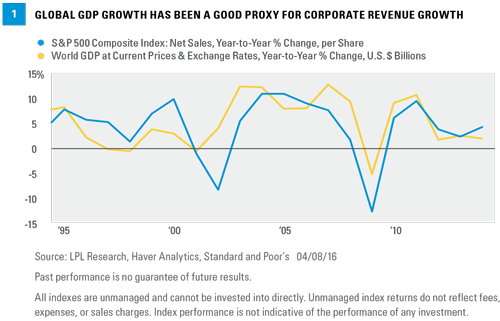

A good proxy for global revenue growth is global GDP growth plus inflation. Thus, the pace of growth in the global economy is a key driver of global earnings growth, and ultimately, the performance of global equity markets [Figure 1]. As we noted in the recent Weekly Market Commentary, “Q1 2016 Earnings Preview: No More Excuses,” the consensus of analysts expects that S&P 500 companies will post a 7% drop in earnings growth in the first quarter of 2016 versus the first quarter of 2015. The expected decline is primarily driven by the stronger U.S. dollar and the decline in oil prices; however, we expect more than a handful of firms may cite global growth concerns (mainly in emerging markets and especially in China) when discussing first quarter results and providing guidance for the second quarter of 2016 and beyond.

GROWTH ESTIMATES ARE ALMOST ALWAYS REVISED LOWER

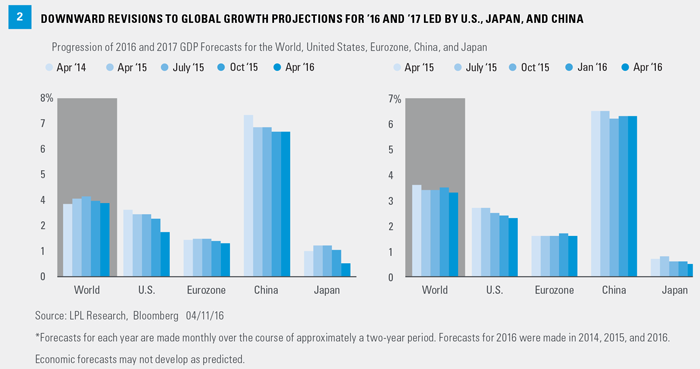

Figure 2 details the progression of the consensus GDP forecasts for 2016 and 2017 for the world, the U.S., China, the Eurozone, and Japan over the past several years. Figure 3 presents the changes over the past six years in the Bloomberg consensus estimate for global GDP for each year from 2011 through 2017, as an extension of the “world” bar. In short, the widespread and frequent reports in the media — most often cited by bearish investors — that “global growth has been revised downward” are technically correct, but miss the point that global growth estimates are almost always revised lower. That pattern could be reinforced this week when the IMF releases its World Economic Outlook. Despite this pattern of revising GDP growth estimates lower, the global economy has been in recovery since 2009, and global equity prices — as measured by the total return on the MSCI World Index — are up 151% since March 2009, and have posted gains in five of the seven calendars years from 2009 through 2015. Year to date through April 8, 2016, the MSCI World Equity Index is down 1.8%.

The latest (mid-April 2016) Bloomberg-tracked economists’ consensus forecast for 2016 global GDP growth stands at 3%, well below the 3.3% expected six months ago in October 2015 and the 3.5% growth expected in April 2015. In mid-2014, when Bloomberg first began tracking consensus estimates for global GDP growth for 2016, the consensus expected 3.8% world GDP growth. The downward revisions to 2016 global growth estimates are nothing new [Figure 3].