We just got through another Berkshire Hathaway shareholders meeting (something I hope to never attend), where Warren Buffett gave us an update on his “hedge funds vs. S&P 500” bet.

So a few things here. Buffett is very cynical and likes to take advantage of people’s stupidity. He also famously bet a billion dollars that nobody would pick a perfect NCAA tournament bracket, which he was mathematically certain to win.

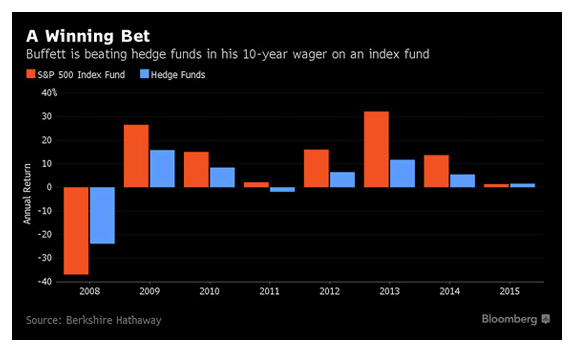

Back in 2008, Buffett made a very loud, annoying bet that the Vanguard S&P 500 index fund would outperform a basket of hedge funds over 10 years. Eight years into the 10-year period, Buffett is winning pretty handily. In the classic understatement we have come to expect from a former Business Insider editor, Joe Wiesenthal said that Buffett is “absolutely crushing it” on his trade.

Indeed he is. Here is the chart.

This bet was a no-brainer from the start. Everyone knows that active managers underperform passive managers in the long run—this is not new. It’s been around since Malkiel and his random walk theory decades ago. Buffett is feeding the prevailing sentiment, which is that Wall Street people are corrupt and dishonest and charge lots of fees and add no value. People believe this because Buffett says it and he has credibility (hopefully they do not take his advice about drinking five Cokes a day).

But I’m going to ask you the same question I asked myself when I read A Random Walk Down Wall Street almost 20 years ago: If it were really true that active management was a fool’s errand, and that the hundreds of thousands of people who work in the money management business add no value, then why does it exist?

Because they do add value.

Have A Coke And A Smile

May 6, 2016

« Previous Article

| Next Article »

Login in order to post a comment