What is that causal narrative? It’s not just the mechanistic aspects of pricing, such that the inherent exchange value of things priced in dollars — whether it’s a barrel of oil or a Caterpillar earthmover — must by definition go down as the exchange value of the dollar itself goes up. More impactful, I think, is that for the past seven years investors have been well and truly trained to see every market outcome as the result of central bank policy, a training program administered by central bankers who now routinely and intentionally use forward guidance and placebo words to act on “the dance of mind” in classic Mephistophelean fashion. In effect, the causal relationship between monetary policy and oil prices is a self-fulfilling prophecy (or in the jargon du jour, a self-reinforcing behavioral equilibrium), a meta-example of what George Soros calls reflexivity and what a game theorist calls the Common Knowledge Game.

The causal relationship of the dollar, i.e. monetary policy, to the price of oil is a reflection of the Narrative of Central Bank Omnipotence, nothing more and nothing less. And today that narrative is everything.

Here’s something smart that I read about this relationship between oil prices and monetary policy back in November 2014 when oil was north of $70/barrel:

I think that this monetary policy divergence is a very significant risk to markets, as there’s no direct martingale on how far monetary policy can diverge and how strong the dollar can get. As a result I think there’s a non-trivial chance that the price of oil could have a $30 or $40 handle at some point over the next 6 months, even though the global growth and supply/demand models would say that’s impossible. But I also think the likely duration of that heavily depressed price is pretty short. Why? Because the Fed and China will not take this lying down. They will respond to the stronger dollar and stronger yuan (China’s currency is effectively tied to the dollar) and they will prevail, which will push oil prices back close to what global growth says the price should be. The danger, of course, is that if they wait too long to respond (and they usually do), then the response will itself be highly damaging to global growth and market confidence and we’ll bounce back, but only after a near-recession in the US or a near-hard landing in China.

Oh wait, I wrote that. Good stuff.

But that was a voice in the wilderness in 2014, as the dominant narrative for the causal factors driving oil pricing was all OPEC all the time. So what about that, Ben? What about the steel cage death match within OPEC between Saudi Arabia and Iran and outside of OPEC between Saudi Arabia and US frackers? What about supply and demand? Where is that in your price chart of oil? Sorry, but I don’t see it in the data. Doesn’t mean it’s not really there. Doesn’t mean it’s not a statistically significant data relationship. What it means is that the relationship between oil supply and oil prices in a policy-controlled market is not an investable relationship. I’m sure it used to be, which is why so many people believe that it’s so important to follow and fret over. But today it’s an essentially useless exercise in data analytics. Not wrong, but useless … there’s a difference!

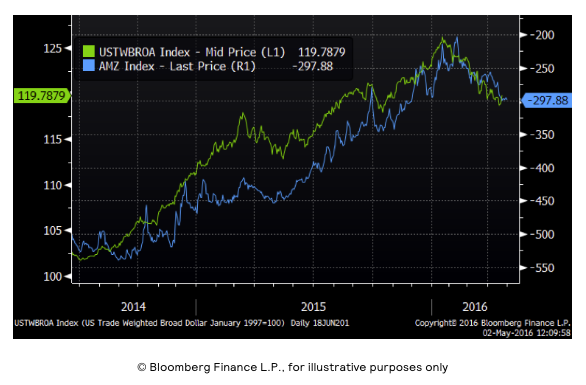

Of course, crude oil isn’t the only place where fundamental supply and demand factors are invisible in the data and hence essentially useless as an investable attribute. Here’s the dollar and something near and dear to the hearts of anyone in Houston, the Alerian MLP index, with an astounding -94% correlation:

Interestingly, the correlation between the Alerian MLP index and oil is noticeably less at -88%. Hard to believe that MLP investors should be paying more attention to Bank of Japan press conferences than to gas field depletion schedules, but I gotta call ‘em like I see ‘em.

And here’s the dollar and EEM, the dominant emerging market ETF, with a -89% correlation:

There’s only one question that matters about Emerging Markets as an asset class, and it’s the subject of one of my first (and most popular) Epsilon Theory notes, “It Was Barzini All Along”: are Emerging Market growth rates a function of something (anything!) particular to Emerging Markets, or are they simply a derivative function of Developed Market central bank liquidity measures and monetary policy? Certainly this chart suggests a rather definitive answer to that question!