KEY TAKEAWAYS

· Corporate earnings, the most important factor in market performance, were poor in developed foreign markets last quarter.

· Forecasts for future earnings have been improving in emerging markets and Europe, but have declined dramatically for Japan.

· Strength out of the German DAX could be one clue that better times are ahead for Europe.

Macroeconomics and geopolitics are interesting to discuss, but earnings are what drive markets. We tend to forget that truism when dealing with international markets. The recent Brexit vote and discussions on how, and even if, the United Kingdom will eventually leave the European Union have dominated the news, and especially social media. However, the biggest problems facing developed foreign markets are not politics or economics, but the inability of non-U.S.-based companies to grow earnings and revenue. In Europe, earnings are falling faster than revenue, though expectations have been improving for growth in both metrics. The earnings picture in Japan remains very troubled. Overall, we are looking for a turnaround in earnings and earnings expectations before becoming optimistic on developed foreign equities.

AMATEURS VS. PROFESSIONALS

There is an old expression in the military that “amateurs discuss strategy, professionals discuss logistics.” For investors, we can translate that to “the macro matters, but ultimately markets move on earnings.” Earnings season is, for the most part, over in the U.S., but we are still in the tail end of earnings for developed international stocks, with 76% of firms reporting as of August 11, 2016. Emerging markets (EM) earnings season is just beginning, with less than half the companies releasing earnings as of this date. We will provide an update on EM earnings in September after more companies have announced results.

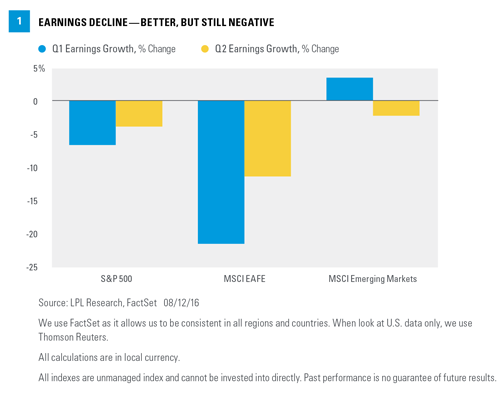

Unfortunately, revenue and earnings in developed foreign markets are in reverse [Figure 1]. If the U.S. is experiencing an “earnings recession,” then overseas stocks are in an “earnings depression.” The decline in both revenue and earnings is surprising. Though both Europe and Japan have economies that are sluggish at best, they have managed to avoid recession. There are many possible culprits for such poor corporate performance, most recently, the uncertainty created by late June’s Brexit vote. The true reasons likely run deeper. The two biggest problems in developed markets are demographics and rigid labor markets, which make hiring and firing workers difficult.

LOOKING THROUGH THE NUMBERS

What matters most to financial markets are not historical earnings, but forecasts for future earnings and how these forecasts evolve over time. Wall Street analysts tend to be overly optimistic about future earnings, reducing forecasts as earnings season approaches. There are two data points related to earnings: the release of current earnings and revisions to future earnings. The current earnings reporting season is following the typical pattern, with forecasts coming down since the beginning of the year [Figure 2]. Two things are striking about this chart. Earnings estimates for emerging market equities in the third quarter of 2016 have increased in the past few months, and the outlook for next year’s earnings are essentially unchanged. However, for developed international markets, estimates for both next quarter and next year have fallen—dramatically.