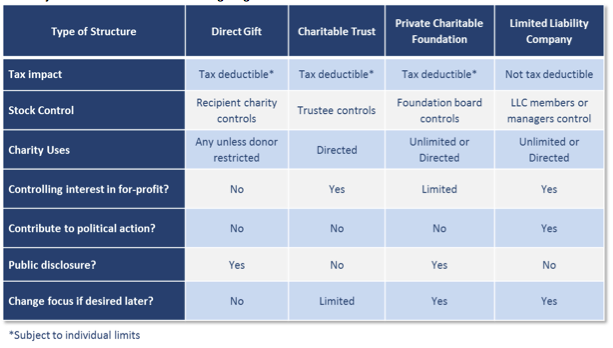

Into the world of revolutionary technology and life-altering wealth are Mark Zuckerberg and Dr. Priscilla Chan! As the founder and primary shareholders of Facebook, they were faced with additional consideration for gifting their shares—financial control of the firm. For most of us, shares gifted outright to a charity generate a tax deduction equivalent to their value at the time of the gift. The charity can then retain the shares or sell them, and upon sale, incur no taxable obligation due to their charitable status. Cleary, the outright gift of the Facebook stock would have had several unsatisfactory results. There is no scenario in which the tax deduction generated by the gift can be effectively utilized. The astronomic income level it would take to use the tax deductions at the highest tax bracket would trigger the alternative minimum tax and wipe out almost all the deductibility of the gift. But far more importantly, in doing this, Mark Zuckerberg would give up financial control of the company he founded. As each charity sold the stock, the financial control he once enjoyed would dissipate across thousands of new individual owners.

In the end, the most logical choice of entity for the Zuckerberg Chan Initiative was a limited liability company. First, the LLC allows the gifts to charitable organizations to be done over time and be modified based on the opportunities available. A charitable distribution isn’t mandated each year, so the LLC can work with charities over time to get them ready to receive larger donations. Second, an LLC can invest in for-profit organizations under the same legal structure and executive managers. This allows for potential investments in public/private cooperative efforts and allows the foundation to harvest the profit motive for positive change. Third, the LLC is controlled by the partners in the LLC or the managers they designate. This allows Mark Zuckerberg to retain de facto financial control of Facebook, and offers complete flexibility to the direction of the LLC going forward. The creation of this initiative will not immediately generate any taxable implications, as an LLC is taxed to the individual partners which created it—so the conversations about skirting taxes is a bit misplaced. The real conversation should be about harnessing a financial structure to achieve the public good and the possible outcomes collaborative problem solving may have on the issues of global poverty, preventable disease and lack of education. Regardless of legal structure, the Zuckerberg Chan Initiative focuses attention on working together to positively impact the world. Creativity led to the Zuckerberg fortune by changing the way we stay connected. Now, we’re about to see how creativity changes the next generation in philanthropy by making new connections.

Robert J. Holton is vice president, Private Client Group at Cleary Gull www.clearygull.com.