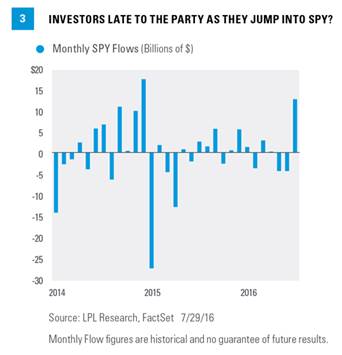

Why Any Pullbacks Will Likely Be Contained

As the risk of increased market volatility becomes higher in August due to seasonal price patterns and increasing bullish sentiment, one saving grace may be the recent improving trend in equity market breadth (as measured by the percent of S&P 500 members with new 52-week highs), which may lessen the impact of a potential equities market sell-off.

We first introduced this market breadth indicator in a blog post entitled “Bullish Market Breadth: Better Late to the Party Than Not Show Up at All” (June 9, 2016). Since then, the three-week average of the percent of S&P 500 members with new 52-week highs has remained above the 6% threshold (currently at 7.1%), which increases the likelihood that this breadth indicator is supporting the beginning stages of a bullish cycle or trend [Figure 4].

Looking at historical weekly data, when the three-week average of the percent of S&P 500 members with new 52-week highs is above 6%, subsequent returns on the index tend to be bullish. Going back to 1990, there were 57 times this happened. Three months later, the S&P 500 was higher 38 times (67% of the time) with an average return of 1.1% and a median return of 2.4%. Going out six months, the returns are higher 46 times (80% of the time) with an average return of 4.2% and a median return of 5.1%. Looking out over 12 months, the returns were higher 51 times (89% of the time) with an average return of 9.9% and a median return of 9.7%.

With the percent of S&P 500 members with new 52-week highs remaining at levels that support the continuation of a bullish price trend for stocks, we view any potential short-term weakness in the equities market as an opportunity to buy on a dip.

CONCLUSION

Seasonality, sentiment, and the coming election could all add to potential volatility over the next few months. From a bigger picture perspective, it is comforting that many sentiment indicators are nowhere near levels seen at past major peaks. Yes, near-term the concerns have greatly increased, as there are many more bulls now, but we don’t see any signs from sentiment readings that would lead us to think the bull market is near an end.

We still expect a better economy in the second half of the year, which we believe may result in total equity returns potentially in the mid- to high-single digits when 2016 is all said and done.* This, along with support from breadth and minimal pressure from improving sentiment, may limit any potential pullback to 5-10%. But put your seatbelts on, as August may provide for a lot more volatility than the second half of July did.

*We expect mid-single-digit returns for the S&P 500 in 2016, consistent with historical mid-to-late economic cycle performance. We expect those gains to be derived from mid- to high-single-digit earnings growth over the second half of 2016, supported by steady U.S. economic growth and stability in oil prices and the U.S. dollar. A slight increase in price-to-earnings ratios (PE) above 16.6 is possible as market participants gain greater clarity on the U.S. election and the U.K.’s relationship with Europe.

Burt White is chief investment officer for LPL Financial.