For many financial advisors, the aging of clients can be detrimental to their practices. When those older clients die or transfer their wealth to their heirs, the financial advisor typically loses their assets.

In a survey we performed of 489 financial advisors, about one-sixth of them lost $500,000 or more when a client died and the children or spouse inherited (Figure 1). Nearly a third of these financial advisors know peers who lost $500,000 or more when a client died and the children or spouse inherited.

Perspectives Of The Wealth Creators

Many strategies are being employed to maintain management of investable wealth during these transitions. Few are proving successful.

A key contributor to the lack of success is failing to understand the thinking of the wealth creators. To address this knowledge gap, we surveyed 179 wealth creators with investable assets ranging between $1 million and $8 million.

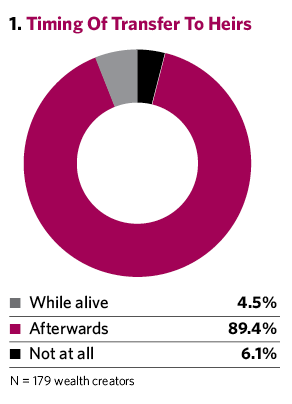

About nine out of 10 of the wealth creators anticipate transferring assets to their heirs when they die. (Figure 1). About 5% expect to transfer their wealth while they are alive. Six percent don’t plan to give to their heirs.

Since the overwhelming majority of wealth creators are giving their money through their estate plans, it’s insightful to realize that fewer than one in five of them has discussed his or her estate plans with heirs. More telling is that nine out of 10 wealth creators believe their heirs do not know the size of their estates.

There are a number of reasons that wealth creators do not discuss their estates with their heirs:

• It’s not a high priority in their family.

• Such discussion would cause problems and arguments.

• It’s not the concern of the heirs.