2016 was a terrible year for the performance of active stock pickers. According to Bank of America Merrill Lynch, 81% of US Large Cap active funds underperformed their benchmark . Although we doubt that stock pickers will continue to underperform quite as badly as they did last year, investors seem to be waking up to the inherent performance problems for traditional active managers. It is difficult for every stock picker to outperform when there are so many stock picking funds and so few managers willing to take sizeable risks within their portfolios.

We are not stock pickers at RBA. We have never made a claim to be able to differentiate stock A from stock B, and will never make such a claim. Rather, our performance is based on meaningful macro positions based on asset allocation, size, style, geography, quality, and other market segments.

Pactive investing, the active management of passive investments like ETFs, is RBA’s specialty. The growing breadth and depth of the ETF market leads us to believe that RBA is uniquely positioned to combine the most important aspects of both passive and active management.

Passive investments are NOT a panacea for poor active management

When we started RBA in 2009, we emphasized that the firm was a manager of beta. Alpha is important, but if one doesn’t make superior beta allocations, then alpha can be totally irrelevant. For example, an active, stock picking manager might outperform a benchmark by several hundred basis points, but if the benchmark’s return was -20%, then the investor nonetheless received a substantial negative return. At RBA, we drive our alpha through beta allocation, i.e., through macro decisions rather than through individual stock selection.

Investors’ returns during the “lost decade” in equities were a perfect example of poor beta management. The widely held view during the late-1990s was that “stocks for the long term” was a winning strategy, and that one couldn’t go wrong with a simple S&P 500® index fund. Unfortunately, the S&P 500R underperformed many other stock indices during the next 10 years. The idea that a passive investment, in this case an S&P 500® index fund, was a definitive route to better returns was clearly wrong because investors had forgotten the most important decision was which index fund to buy and when!

Today, ETFs are considered a solution to inferior active returns, but the problems regarding which ETF to buy and when to tactically buy them will likely continue to be a significant challenge. Chart 1 shows the relative performance between small cap and large cap US stocks (the Russell 2000® vs. the S&P 500®). Small caps were outperforming large caps when the line is going up, and vice versa. Small cap relative outperformance peaked in mid- 1984, and then proceeded to underperform for most of the next 15 years. Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

One might say this is an extreme and very long-term example, but there are many shorter-term examples we could cite. Chart 2 shows a more recent example between Emerging Market stocks and US stocks. Coming out of the 2008 bear market, most asset allocators favored Emerging Market stocks over US stocks. However, a portfolio allocated to Emerging Markets anytime from 2008 to 2011 would have significantly underperformed one allocated to US stocks. Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

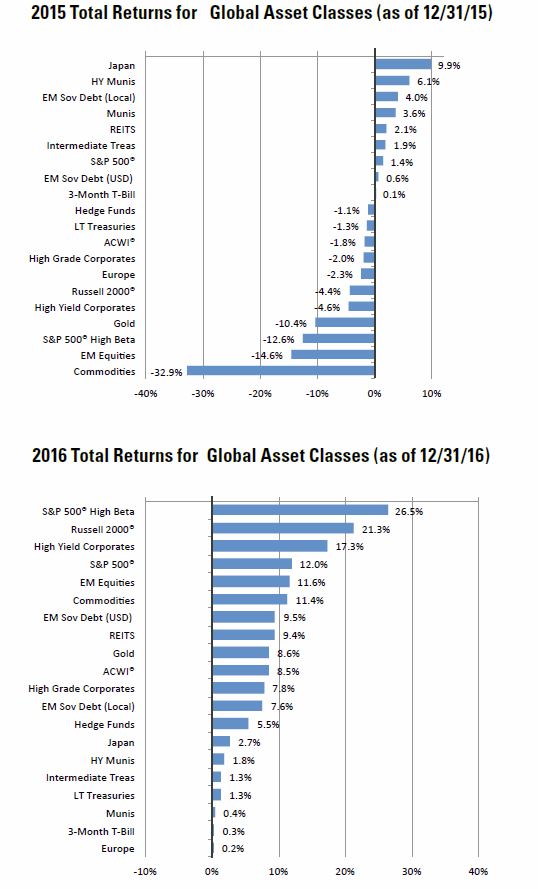

Although many profess to be “long-term investors”, the turns in asset class leadership can be very meaningful even year by year, and often have a backward-looking effect on investor positioning. Chart 3 shows asset class performance during 2015 when global profitability was waning versus asset class performance in 2016 when global profitability was accelerating. Some of 2015’s worst performing asset classes became 2016’s best performers. Investors should clearly have a long-term strategic investment plan, but tactical allocation can have a consequential impact on portfolio performance.

Source: Richard Bernstein Advisors LLC, MSCI, HFRI, Standard & Poors. BofA Merrill Lynch, Bloomberg. For Index descriptors, see “index Descriptions” at end of document.

Anyone can do this!...Maybe not.

One might think that allocation of ETFs is easier than picking active managers, and therefore, anyone can be a Pactive® manager. Several points suggest otherwise: