The United States has been under a “recession warning” for two years now. And after a brief lull as we entered 2024, the alarms are sounding again. It’s not the usual suspects of an inverted Treasury market yield curve or low consumer and business sentiment. Instead, some economists worry that the rising unemployment rate in several states means a recession is coming - or even here already.

The basis for these warnings is a highly accurate recession indicator I developed that has become known as the Sahm rule. As I have explained before, the premise is simple. If the three-month average of the unemployment rate (the monthly rate often bounces around too much) is half a percentage point or more above its low in the prior 12 months, the economy is in a recession.

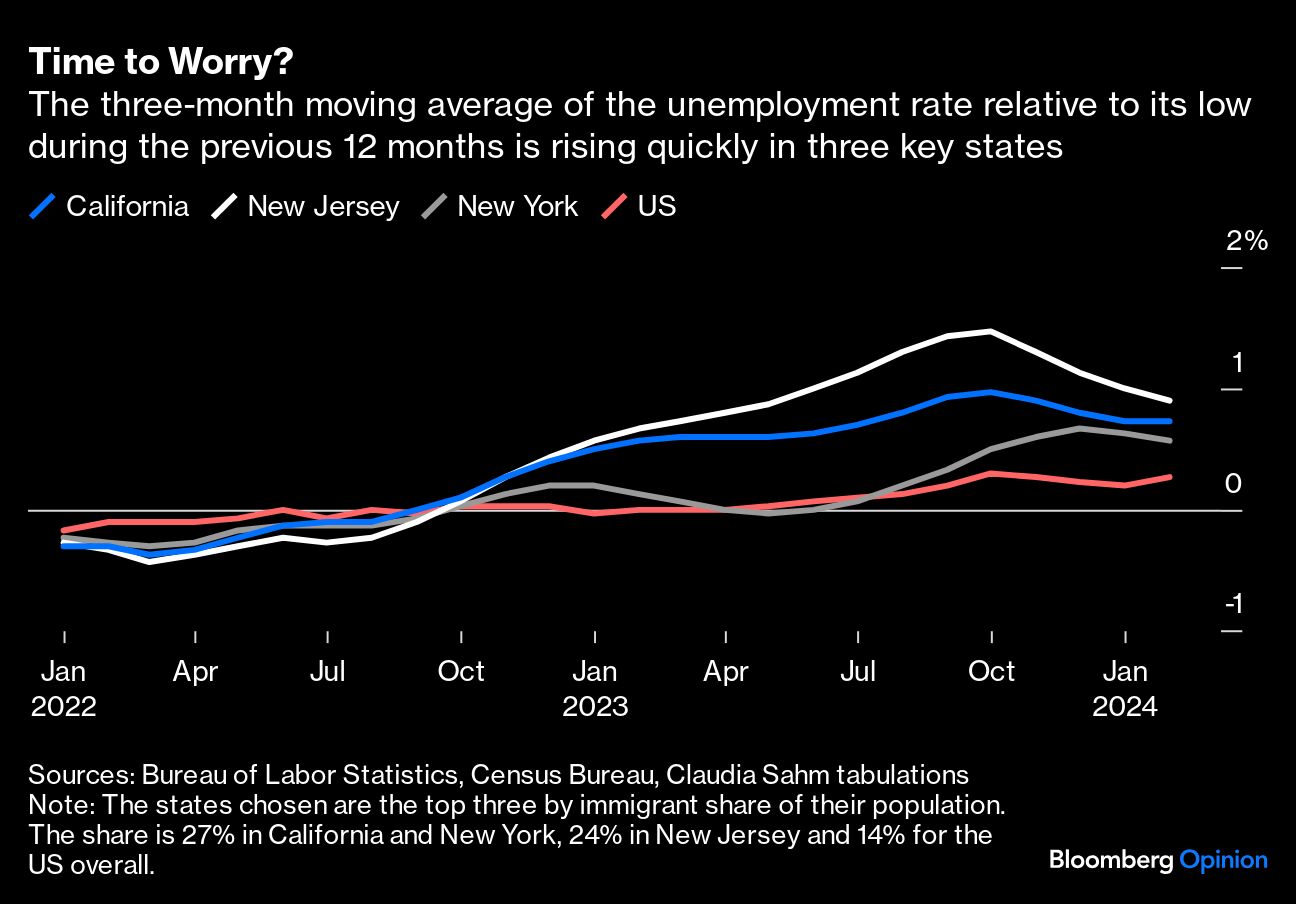

Applying the logic of the rule to individual states would reveal that 20 of them should be in a recession, right? After all, these states account for more than 40% of the US labor force and includes California, which alone has 11%.

Although this may appear dire, the increase in unemployment rates stem partly from the strength of the economy the past few years, strength that has attracted much needed immigration to meet the demands of a hot labor market. According to the Congressional Budget Office, net immigration totaled 2.6 million in 2022 and 3.3 million in 2023, rising from an average of 900,000 a year from 2010 to 2019.

As immigrants enter the economy, especially in large numbers, it can take them time to find work — likely even longer than US-born new entrants to the labor force. Moreover, immigrants have higher labor force participation rates overall than US-born individuals. The immigration process itself can create delays in legal employment, especially for humanitarian parolees and asylum seekers. More generally, an increase in the labor force has been long understood to be a “good” reason for why the unemployment rate temporarily rises as new workers find jobs.

Indeed, the national unemployment rate drifted higher, from 3.5% in July to 3.9% in February, along with increased immigration and other new entrants to the labor force, such as women, people of color, and people with disabilities. However, immigrants are not evenly spread across the country, so the national drift upward in unemployment has been more pronounced in certain states. The three with highest immigrant share in their state population — California (27%), New Jersey (24%), and New York (27%) — have some of the largest increases in unemployment. They also account for 20% of the US labor force.

And consistent with an adjustment to a larger labor force — as opposed to a recessionary spiral — the unemployment rate in these states has come down from their peaks last year.

But what does all this mean for the economy? Some say more jobs going to immigrants the past few years than those born in the US is a problem. The reality is that immigrants solved an unusual issue created by the Covid-19 pandemic. Almost three million workers left the labor force early in the pandemic. Older adults who chose to retire were a large part of that group, as were women with children. Many were slow to return, and the aging of the population led to further retirements.

So, in 2021, when the economy re-opened and consumers came back strong, the economy experienced a shortage of workers. Recall that through most of 2021 and 2022, labor shortages dominated the headlines and created intense competition for workers, leading employers to raise wages and then pass those extra costs to consumers, which helped to elevate inflation. For its part, the Federal Reserve was concerned the labor market was running too hot, with around two job openings for every unemployed person, and raised benchmark interest rates at an unprecedented pace.

Immigrants filled jobs and were crucial to solving the labor shortage. In 2022, the foreign-born labor force was 1.4 million larger than before the pandemic and 2.7 million larger in 2023, far exceeding the sluggish recovery in the US-born labor force.

Research in the past has shown that new immigrants were unlikely to compete with US-born citizens for jobs because of their different skill sets. In addition, the recent labor shortages suggested that immigrants were filling jobs, not taking them from other workers. Resolving the labor shortage takes pressure off inflation. Immigration has also boosted gross domestic product, as Wendy Edelberg and Tara Watson, economists at the center-left Brookings Institution, showed in a recent report. We know that the economic recovery in the US is far outpacing peer countries, partly due to more workers from immigration.

The economic contributions of immigrants during this recovery — reducing the labor shortages, taking pressure off inflation and adding to output — are often overlooked. In fact, more than 40% of Americans, according to a Gallup poll, say the level of immigration it too high. But reducing immigration would be a step backward for the economy. The patterns in unemployment across states reveal the important role of immigrants in re-balancing of the labor market. The story of the economy since the pandemic began has been unlike anything in the past. Applying the Sahm rule to state unemployment rates without asking why the rates are rising and assuming the worst is a mistake.

Claudia Sahm is the founder of Sahm Consulting and a former Federal Reserve economist. She is the creator of the Sahm rule, a recession indicator.

This column was provided by Bloomberg News.