A change of seasons should be noted by municipal investors, as a seasonal increase in new issuance may be a catalyst to lower returns after a strong 2014.

A change of seasons should be noted by municipal investors, as a seasonal increase in new issuance may be a catalyst to lower returns after a strong 2014.

It is not uncommon for revenues to slow as the economy matures, and we do not view the slowdown in state tax revenues as worrisome for municipal bond investors.

This week marks the start of fall with the autumnal equinox. In coming weeks, nighttime hours will gradually surpass daytime hours throughout the United States. Similar to the shift in the number of daytime and nighttime hours, state revenues have evened in recent months and the upside surprises of recent years are fading.

After several years of growth, state tax revenues are slowing. The Nelson A. Rockefeller Institute of Government reported that overall state tax revenues declined by 0.3 percent during the first quarter of 2014, and a preliminary reading for the second quarter 2014 shows tax revenues are on track to decline by 0.8 percent. A drop in personal income taxes drove declines while sales taxes and corporate income taxes, the two other major drivers of state tax revenue, continued to increase. A spike in tax collections in 2013, following an increase in tax rates, is the main driver of slowing personal income taxes as it makes year-over-year comparisons more challenging. The surge in 2013’s revenue gains was unlikely to be sustained.

It is not uncommon for revenues to slow as the economy matures and we do not view the slowdown in state tax revenues as worrisome for municipal bond investors. Withholding taxes, a more current gauge of the trajectory in revenues, increased 5.6 percent during the first quarter of 2014 with 37 states showing gains and only four showing declines. Personal income taxes consist of both income and investment taxes and therefore can fluctuate depending on strength in the stock market. Measuring withholding taxes can therefore provide a clearer picture of the underlying trend in personal income tax revenues. For the first three quarters of fiscal year 2014 (which began on July 1, 2013), revenues have increased 2.8%. We would have to witness much sharper revenue declines before default risk may become a factor again in the municipal bond market.

California, New Jersey And Illinois

For the new 2015 fiscal year that began July 1, the flat overall revenue trend appears to be continuing based upon a small subset of sampling. Revenues have been a mixed bag with states such as Idaho, Indiana, Vermont, Wisconsin, New Jersey, Florida, Minnesota, Arizona, and Virginia slightly lagging budget forecasts, while California, Maine, Missouri, and Washington have been modestly exceeding forecasts.

Among notable state progress, California’s revenues continue to improve while New Jersey and Illinois face challenges. California state general obligation (GO) debt was upgraded to Aa3 in June 2014 by Moody’s as a reflection of the better revenue picture and followed upgrades by both Standard & Poor’s (S&P) and Fitch in 2013. Conversely, New Jersey state GO debt has been downgraded more than once in 2014 and most recently here in September by both S&P and Fitch, as revenues disappoint and the state’s pension burden continues to grow. Illinois not only has the lowest pension funding level among states but also faces a decline in revenue as a temporary increase in tax rates, which helped boost Illinois debt back in 2011, is set to expire at the end of 2014 and revert back to lower rates—a negative for bond holders. While Illinois state GO debt trades at a notable yield premium to the average AAA-bond yield, New Jersey debt yields are relatively narrow to the AAA average and yield differentials may widen to compensate for risks. Meanwhile, California has seen its bonds outperform as yield differentials narrow.

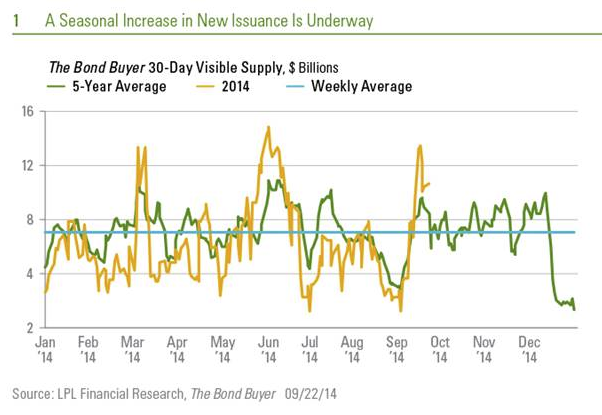

A Change In Season For Supply

Slowing revenue growth is likely to increase the chance the low supply environment of 2014 will persist, but a seasonal increase is currently underway. As is typically the case, the start of fall ushers in a period of increased issuance [Figure 1]. New bond issuance has been very low in 2014 but has still tracked the pattern of the recent five years. Each of these years has held very close to the seasonal pattern with some slight variation. In 2010, issuance was well above average and, along with credit quality fears, sparked a subsequent year-end sell-off, while 2013 fall issuance was slow to get going due to the taper tantrum sell-off and lingering market caution.

At $11.3 billion, forward issuance remains well above the $8.2 billion weekly average of the past five years and may slow municipal performance. Municipal bonds outperformed Treasuries during a two-week bond market downturn to start September. Although bond prices rebounded slightly last week, the combination of lower yields and higher valuations may slow, or reverse, the advance of municipal bonds.

Municipal-to-Treasury yield ratios are near their most expensive indications of the year [Figure 2]. We do not expect a repeat of the 2013 sell-off, but after a strong start to 2014, the combination of lower yields, higher valuations, and a seasonal increase in supply may drive much lower returns. Returns may gravitate closer to the negative 0.3 percent return of the Barclays Municipal Bond Index witnessed from August 29, 2014 through September 19, 2014 than the 7.5 percent witnessed year-to-date through the end of August 2014.

Once the seasonal supply surge fades, slower state revenue growth and still tight local government budgets suggest that new issuance may remain subdued over the longer term. Therefore, lower issuance may lead to still higher valuations for municipal bonds as supply remains constrained. Data from the Federal Reserve released last week showed the municipal market shrank by 0.2 percent during the second quarter of 2014, continuing a trend that began in 2010. However, over the near term higher valuations may present a challenge in the face of a seasonal supply increase.

A change of seasons should be noted by municipal investors, as a seasonal increase in new issuance may be a catalyst to lower returns after a strong 2014.

Anthony Valeri has been with LPL Financial since June 1993. As Senior Vice President and Market Strategist, Valeri is a member of the Research department’s tactical asset allocation committee and is responsible for developing and articulating fixed income and general market strategy.

The State Of States

September 25, 2014

« Previous Article

| Next Article »

Login in order to post a comment