How do you determine the “safe” portfolio withdrawal rate (what I call “SAFEMAX”) for clients at the beginning of retirement? My research over many years indicates that an initial withdrawal rate of 4.5% sustained all portfolios from 1926 up until now (when we assume that you had a tax-advantaged account, annual CPI adjustments and a minimum of 30 years of portfolio longevity).

But that is based on a “worst case” scenario—for the individual who retired on October 1, 1968, and suffered through years of poor stock market returns and high inflation. Retirees facing more favorable market circumstances, on the other hand, have been able to successfully withdraw up to 13% of their portfolios. So how do we determine a safe withdrawal rate that fits a particular environment—one hopefully significantly higher than 4.5%?

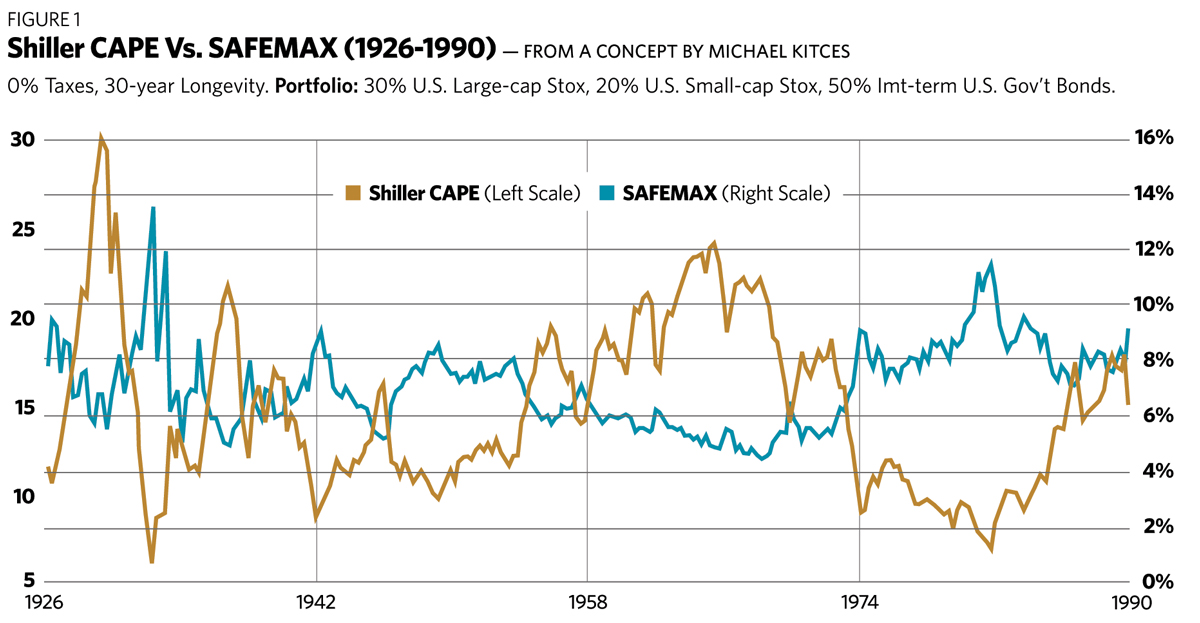

To begin our quest, I am privileged to present an updated version of what I consider to be the single most important chart ever devised pertaining to “sustainable withdrawals” (Figure 1). It was created by Michael Kitces, the renowned financial advisor, and it first appeared in his publication “The Kitces Report” in May 2008. This chart plots the Shiller CAPE (the cyclically adjusted price-earnings ratio for the S&P 500) against the “safe” historical maximum withdrawal rate for the first day of every quarter, from 1926 through 1990, which adds up to 260 scenarios.

First, a few definitions (they may be superfluous, but let’s be certain we are on the same page). The “Shiller CAPE” was devised by Professor Robert Shiller of Yale University. This metric represents a P/E for all the companies in the S&P 500, based on their current stock prices and the previous 10 years of inflation-adjusted earnings. It seeks to “smooth out” short-term fluctuations in earnings and come up with a P/E representative of the true earning power of the companies involved.

“SAFEMAX” is a term I devised in my own research. It represents the highest first-year withdrawal rate (the dollar withdrawal divided by initial portfolio value) that historically sustained a retiree’s portfolio for a given period of time—in this case, 30 years—when the portfolio was tax-advantaged. The rebalancing is annual, and the target portfolio consists of 30% U.S. large-cap stocks, 20% U.S. small-cap stocks and 50% intermediate-term U.S. government bonds.

I have updated Michael’s chart to incorporate recent data. Note that in my analysis I used retirement dates on the first day of each quarter, while Michael’s original chart used annual retirement dates. As a result, my chart has many more data points, and shows more of the “fine structure” of the relationship between CAPE and SAFEMAX. Because 30 years of data is required, the most recent retirement portfolio begins January 1, 1990 (and ends December 31, 2019).